ABC Analysis: A Strategic Approach to Inventory Management

Efficient inventory management is a crucial aspect of running a successful business, irrespective of its size or industry. To achieve this balance, businesses often employ various inventory management techniques, and one of the most effective methods is the ABC Analysis. In this article, I explore the ABC Analysis method, its benefits and best practices.

What is ABC Analysis

The ABC analysis, also known as the ABC classification, is a method used in inventory management to categorize items based on their relative importance to the business. It was first introduced by H. Ford Dickey in 1951 and has since become a fundamental tool for supply chain professionals.

ABC categories

The primary objective of ABC methodology is to help businesses allocate resources efficiently by classifying items into three categories: A, B, and C.

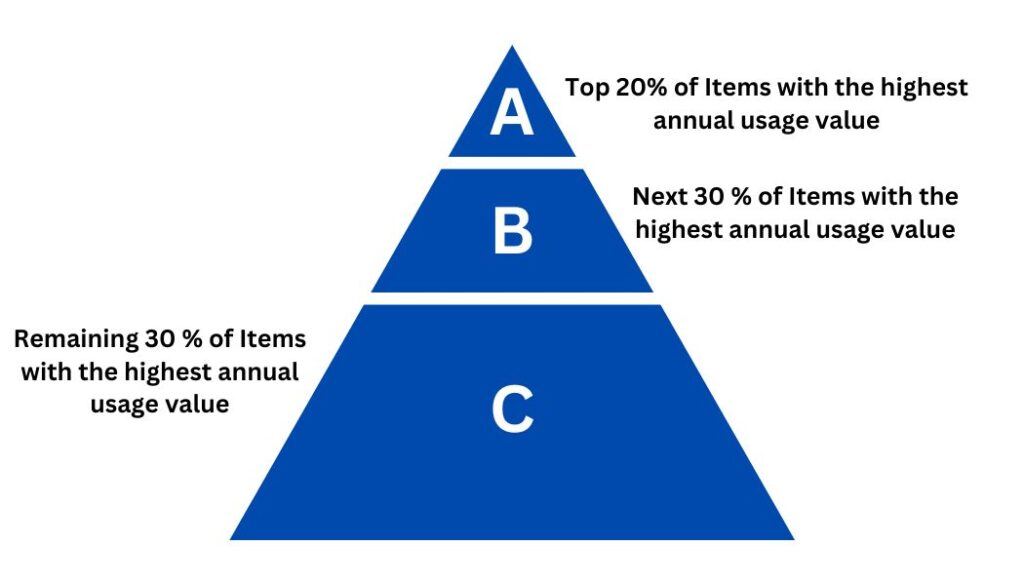

Category A: High-Value, High-Priority Items. These items represent a relatively small percentage of the total inventory but account for a significant portion of the total value. Category A items are critical to the business because they generate a substantial portion of the revenue. Businesses should closely monitor and manage these items to ensure they are always available and avoid stockouts.

Category B: Moderate-Value, Moderate-Priority Items. Category B items fall between Category A and Category C in terms of value and importance. They are important but not as critical as Category A items, and may constitute a moderate portion of the inventory value. Maintaining a balance between ordering and holding costs is crucial for Category B items.

Category C: Low-Value, Low-Priority Items. These items make up a significant portion of the inventory but have a relatively low value. While they are necessary for various reasons, they do not impact the overall financial performance. Businesses should aim to minimize carrying costs for Category C items.

Calculating the ABC Categories

Grouping the products into the ABC categories involves following steps.

1. Determine the Measurement Criteria

Before starting any analysis, you need to decide on the criteria for measuring the importance and value of inventory items. Typically, two primary factors are considered:

- Annual Usage or Demand (U): This represents how frequently an item is sold or used in production over a specific period, often a year.

- Item Cost (C): Item cost is the cost of acquiring or producing an item, often calculated as the purchase price or production cost per unit.

2. Calculate the Annual Usage Value (U * C)

For each inventory item, multiply its annual usage (U) by its cost (C) to calculate the annual usage value (UV). This value reflects the contribution of each item to the total inventory value.

3. Rank the Items by Annual Usage Value

Create a ranked list of inventory items by sorting them in descending order based on their annual usage value, from highest to lowest.

4. Assign Categories: Divide the ranked list into three categories based on your desired criteria. The specific percentages for each category can vary depending on your business needs, but a common breakdown is:

Benefits of ABC Analysis

Using ABC methodology can offer several advantages for businesses:

- Improved Inventory Management: The ABC technique helps companies allocate resources more efficiently. Focus resources on the A items, streamline processes for B items, and simplify controls for C items.

- Inventory Reduction: By categorizing items based on importance, companies can identify opportunities to reduce inventory holding costs, especially for low-priority items.

- Enhanced Planning and Forecasting: Accurately predict demand and optimize purchase orders based on item categories.

- Enhanced Cash Flow: Reducing excess inventory and concentrating resources on high-priority items can improve cash flow by reducing tied-up capital.

- Inventory Turnover: Implementing the ABC classification can lead to a higher inventory turnover rate, allowing businesses to sell and replace inventory items more frequently.

Best Practices for Implementing ABC Analysis

An effective implementation of ABC requires careful planning and attention to detail. Here are some best practices to ensure success:

Focus on clear and objective criteria for classification. Use consistent metrics like annual demand and cost, or gross profit margin, depending on your business goals. Avoid over complicating the analysis with too many factors.

Align classifications with service levels: Assign different service levels (e.g., lead times, safety stock) based on each item’s category. A items deserve stricter controls and faster replenishment compared to C items.

Use technology: Leverage inventory management software to automate the analysis and track changes over time. This practice simplifies the process and ensures accuracy.

Review and update regularly: Don’t consider your ABC classification static. Review it periodically to reflect changes in sales trends, product profiles, and supplier reliability.

Go beyond the 20/30/50 rule: Adjust the percentages if this rule does not reflect your inventory. Experiment and find the percentages that work best for your business.

Use ABC for specific tasks: Apply this analysis beyond inventory management. Use it for cycle counting, prioritizing purchase orders, negotiating with suppliers, and managing warehouse layout.

Integrate with other inventory management techniques: Combine ABC with other methods like safety stock planning, forecasting models, and demand analysis to optimize your inventory control systems.

I hope this article has been helpful to you. I will continue to post information related to warehouse management, distribution practices and trends, and the economy in general. If you are interested in learning more, click the link, and we will call you.

There is a lot of relevant information on our channel. Check this video on the 5 hardest things to implement in a WMS.

Sorry, the comment form is closed at this time.